|

|

....... |

TIMELINE

This web page explains why a simple thing like a timeline can make or break a plan for the future.

Somewhere on this timeline there is a likelihood of certain events, such as a catastrophic health event or the need for long term care.

Planning Age

Our experience working with clients has given us quite a few chances to see individuals who live longer than they originally thought, or longer than their children thought would be possible.

This longevity is somewhat predictable even as the population is increasingly getting older and breaking boundaries in terms of how long people really live.

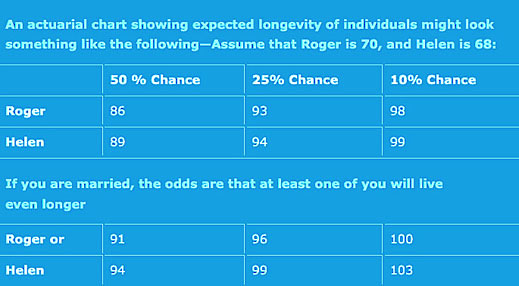

The chart shows the expected chance that Roger and Helen will live to be a certain age. There is a 50% chance that Roger will live to 86, a 25% chance he will live to 93 and a 10% chance he will live to 98. Helen's numbers show that a woman is expected to outlive a man. In the married scenario, the odds that one of them will live to be over 100 is over 10%.

The Planning Age must be realistic and take into account the ongoing longevity of the population.

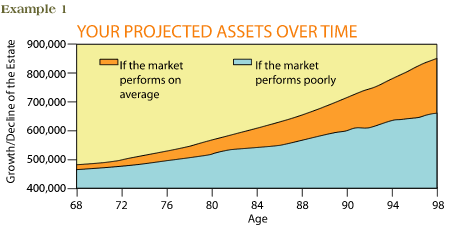

EXAMPLE #1: The plan works

Roger and Helen, a married couple, have $500,000 in savings, investments, and retirement accounts. Their goal is to live in their own home as long as they can and leave a nice estate size to be divided among their heirs. They retire at 63 and 67, and the next 25 years work out very well: Neither falls ill with an incapacitating disease, neither outlives their long term care insurance, their home value goes up and only up, and their fixed incomes are tied to inflation so that the COLA increase meets the real costs of a visit to the supermarket or gas pump. Roger and Helen die rich and are able to leave a healthy estate to their heirs.

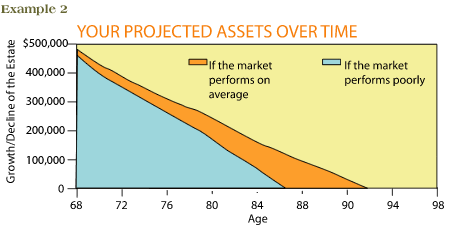

EXAMPLE #2: The plan doesn't work

Roger and Helen don't fair as well. Roger falls ill, outlives the meager LTC insurance he has, and ends up in long term care. The income isn't tied to a realistic COLA, and declines in real dollar terms. The investment counselor misunderstands market risk and the portfolio tanks. The at-home spouse Helen fights the financial fight for awhile, then in a stroke of bad luck has her own debilitating moment in part due to the stress. She too ends up in a private pay care giving situation. Even so, neither passes away and the LTC days pile up. Both live deep into the 80s and mid 90s. Within 7-10 years the savings are gone, the house has been sold, and the second window of money is closing. Upon death the estate has been depleted, the children are bitter and now entering their own 'golden years' with not much family help to help them through. Regretfully, at death is the opposite result of what Roger's and Helen's original intent.

Conclusions

These two scenarios are the opposite ends of a set of possibitlities. Most folks given the same circumstances and goals will end up somewhere in the middle of these two extremes.

Review Our Advance Planning Services for more information about how we can help create the right plan for you based on your expected Timeline and financial circumstances.

Call us at 888 789-4589 to discuss your unique situation.

Website by designwestgraphics.com

|